At BankSouth, we value the trust you place in us to safeguard your money and work every day to ensure you have easy and secure access whenever you need it.

BankSouth has been helping business owners launch and grow their businesses in the community for generations. Whether you’re opening a new location or expanding your existing one, we’re ready to help.

For over ten years, BankSouth has helped thousands of families finance their homes. We know how daunting this may be, but we take the worry and hassle out of the process.

The organization that governs the ACH Network, NACHA, has implemented new requirements that directly impact businesses like yours. Here's what's changing, why it matters, and what you need to do. What's Changing? Under the updated NACHA Operating Rules, banks are...

ATHENS, GA - BankSouth is pleased to announce that Mason Banks has rejoined the Watkinsville team as a Jr. Relationship Manager, serving clients throughout the Watkinsville and Athens area. In his new role, Banks will work directly with clients to understand...

Summer is around the corner, and scammers are already hard at work. From fake Masters tickets to bogus vacation rentals and traffic court scams, fraudsters are finding new ways to cash in. Here's what to watch out for so you...

Media Contact: Bryce McCuin, Director of Marketing [email protected] (706) 454-2319 For Sequence Holdings: Nathanial Garnick/Jonathan Warren Gasthalter & Co. [email protected] Partnership embraces human-first approach to community banking, combining BankSouth’s 80 years of excellence with frontier technology to drive growth and...

Each year, BankSouth holds Kickoff to do one thing: create clarity. But before strategy is discussed and numbers are reviewed, it starts with something simpler, bringing our people together. Across markets and departments, Kickoff gives us time to reconnect, share perspectives,...

In the past 5 years, the Georgia Department of Revenue has blocked over $1.07 billion in fraudulent tax returns. As we move through tax season, fraudsters are working just as hard as taxpayers. This month's Fraud Watch highlights modern tax...

ELLABELL, GA - BankSouth is pleased to announce the addition of Nichole Hearn as Business Development Officer for the BankSouth@Work program, based at the company's Hyundai Motor Group Metaplant America (HMGMA) banking center in Bryan County. With more than two decades...

In April 2025, BankSouth announced its partnership with Hyundai Motor Group Metaplant America (HMGMA) to provide dedicated banking support to the Metaplant workforce, known as Meta Pros. By January 2026, that commitment grew into something permanent — the grand opening of a full-service BankSouth Banking Center inside the Bryan County facility. ...

Start Using Our Template! In a world filled with endless possibilities and financial pressures, it's easy to feel like your money is controlling you rather than the other way around. From unexpected bills to ambitious savings goals, managing your finances...

At BankSouth, community partnerships are not about signage or symbolism. They are about showing up, listening, and helping build something that will matter long after the ribbon is cut. This fall, members of the BankSouth team stepped inside the newly...

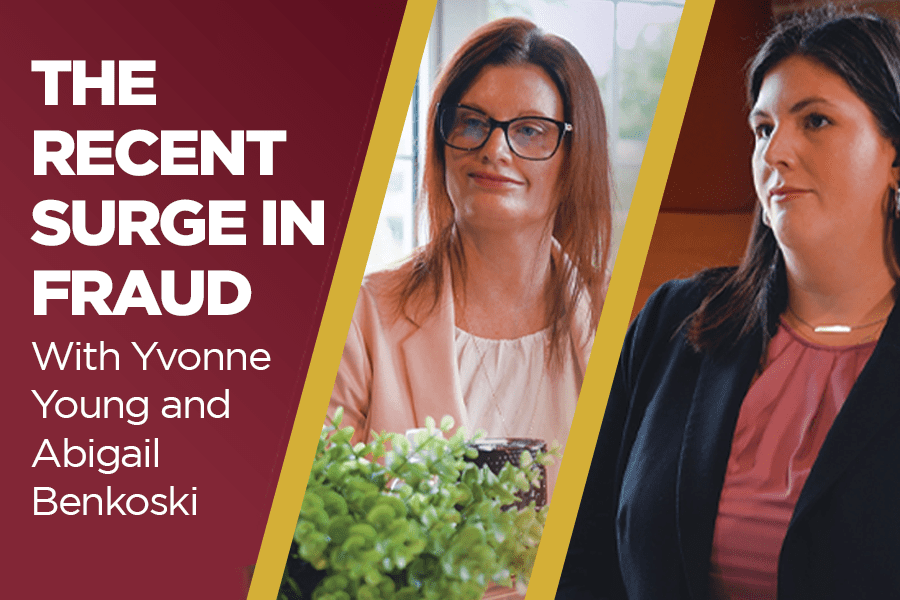

Fraud losses grew 25% from 2024 to 2025, according to the FTC. Fraudsters are always coming up with new ways to catch people off guard. Lately, we’re seeing more fake purchase alert texts, credit repair offers that promise fast results,...

ELLABELL, GA – BankSouth hosted a grand opening celebration on January 22, 2026, marking the official launch of its new on-site banking branch plus ATMs located inside the Hyundai Motor Group Metaplant America (HMGMA) facility in Ellabell, GA. While the...

SAVANNAH, GA – BankSouth is pleased to announce the addition of Mark McRae as Relationship Manager at its Savannah branch. With more than 34 years of commercial banking experience, McRae brings deep market knowledge, proven leadership, and a strong commitment to serving...

As the year comes to a close, scammers ramp up their efforts, taking advantage of seasonal job searches, holiday excitement, and increased online activity. Fraudsters often rely on urgency, pressure, and unfamiliar technology to trick people into acting quickly. Being...

Inside the Fraudcast The BankSouth Fraudcast returns with another conversation focused on protecting our customers, communities, and employees from evolving financial threats. In this episode, Bryce McCuin, Director of Marketing at BankSouth, is joined by Dawn Taylor, Chief Credit Officer,...

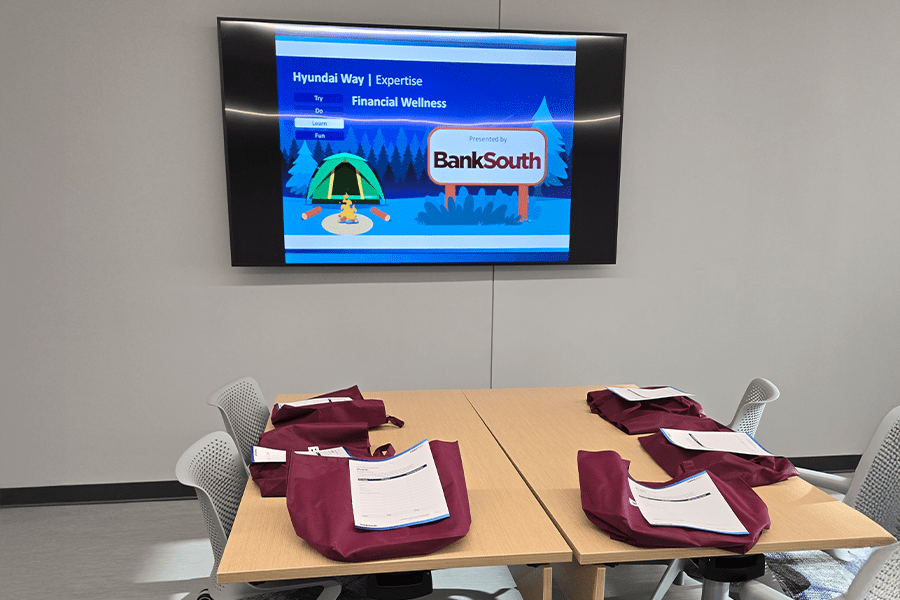

A Shared Commitment to Financial Wellness Beginning in November 2025, Meta Pros at the Hyundai Motor Group Metaplant America (HMGMA) have been taking part in Financial Wellness classes designed to strengthen their financial confidence and long-term success. These sessions are...

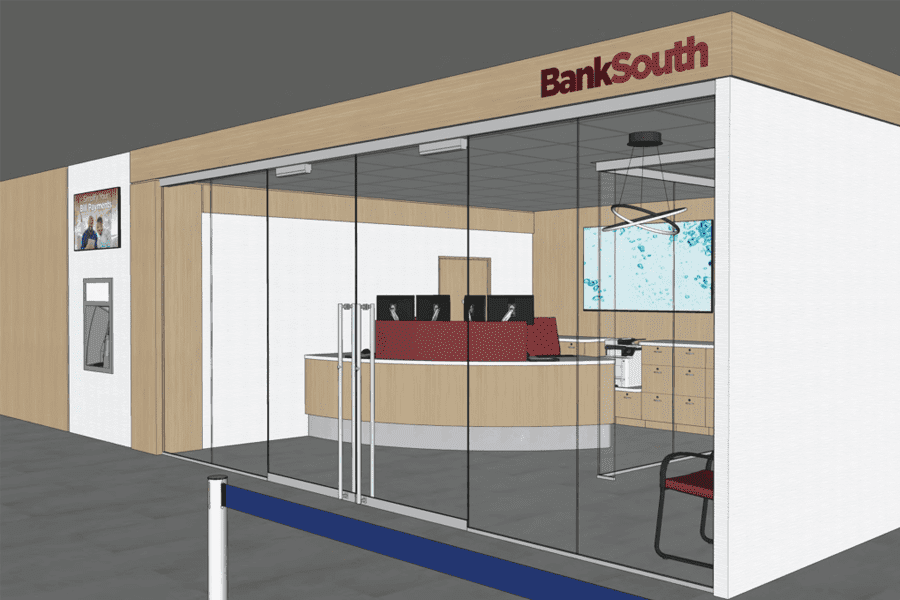

We’re excited to share with you the first looks at our renderings for BankSouth’s on-site branch that will be located within the Hyundai Motor Group Metaplant America facility in Ellabell, Georgia. This dedicated space will support Hyundai’s Meta Pros with...

The Penny’s Final Chapter In May 2025, the U.S. Treasury confirmed what many had long anticipated: the penny’s production has officially come to an end. The final U.S. penny was minted on November 12, 2025, closing a chapter that began...

Inside the Fraudcast The BankSouth Fraudcast continues its mission to bring real-world perspectives on fraud prevention from those working to protect our communities every day. In this episode, Bryce McCuin, Director of Marketing at BankSouth, speaks with Sheriff Donnie, Greene...

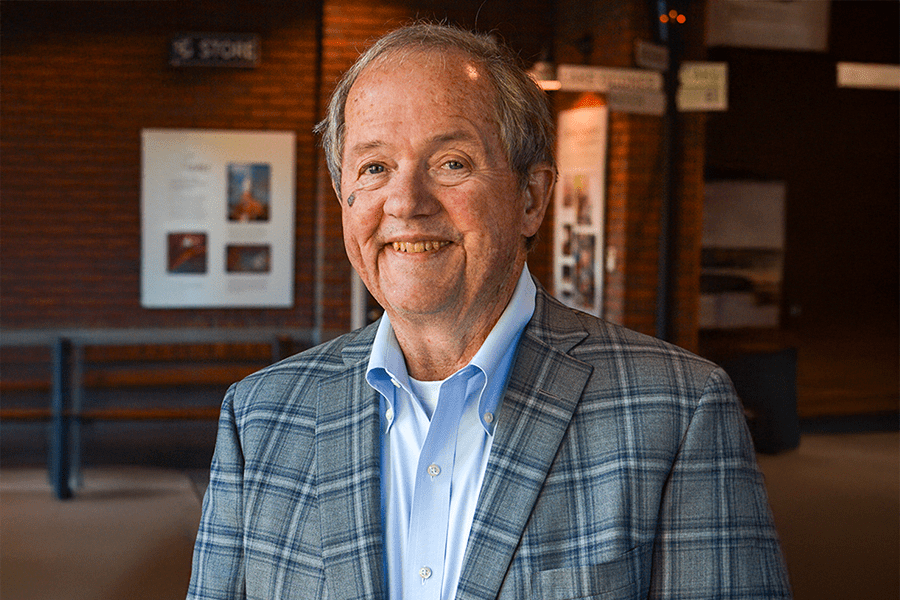

GREENSBORO, GA – BankSouth is proud to announce the appointment of John Phillips to its Board of Directors. Phillips brings more than five decades of distinguished experience in law, business, and community leadership to the BankSouth Board. A graduate of...

Spoof Calls Bank spoof calls happen when scammers disguise their phone number to make it look like your bank is calling. The caller ID may even display the bank’s real name or number. During the call, the fraudster often claims...

Inside the Fraudcast The BankSouth Fraudcast is a podcast series where experts are invited to share real-world insights on protecting your finances. Hosted by Bryce McCuin, Director of Marketing at BankSouth, the series features conversations with subject-matter experts across the...

Savannah, GA – BankSouth is proud to announce the celebration of 10 years in the Savannah market, marking a decade of serving customers, supporting local businesses, and giving back to the community. Since opening its doors in 2015, the Savannah...

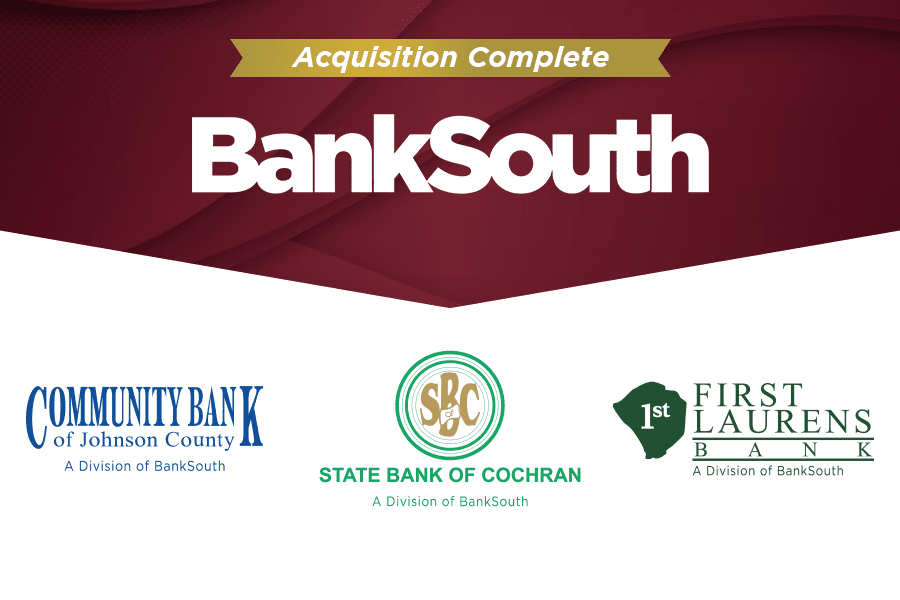

GREENSBORO, GA – On October 1, 2025, BankSouth announced the successful completion of its acquisition of State Bank of Cochran, including its divisions First Laurens Bank and Community Bank of Johnson County. The acquisition brings together long-standing Georgia community banks,...